Last year’s lockdowns, work-from-home, and virtual schooling had people hyper-focused on finding more space and bigger homes. In the third and fourth quarters, as markets reopened, extreme buyer demand set historic sales records that carried over into 2021. With depleted listing inventory—less than half typical levels buyers pounced on fresh listings as soon as they arrived. Multiple quick over-asking-price offers continued to set monthly historic records for both price and speed of sale. In the second week of April, 64% of new pending had been on the market for less than ten days and the average market time for all pending was 17 days.

While sales and prices continue to rally, demand is mellowing. Inventory levels that had dropped for 11 consecutive months began to rise in April. While the fresh listings provided needed fuel for the market and helped the sales run to continue, many of the buyers that had been waiting to find a home have found it and are no longer looking. Days on market, which sits at 17 days should rise. From March through early May, over 60% of new pending were on the market for ten days or less. That percentage has dropped to around 35%.

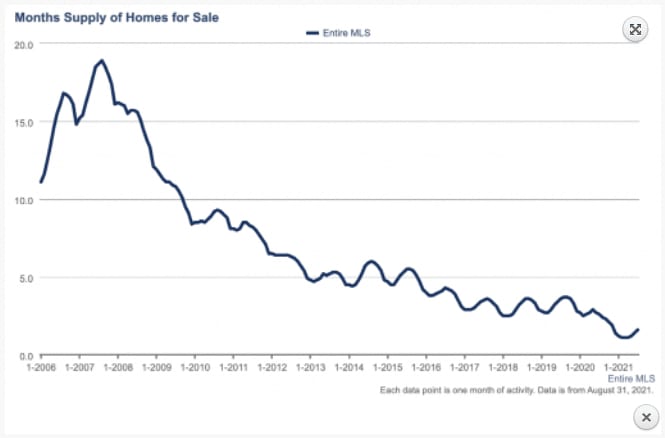

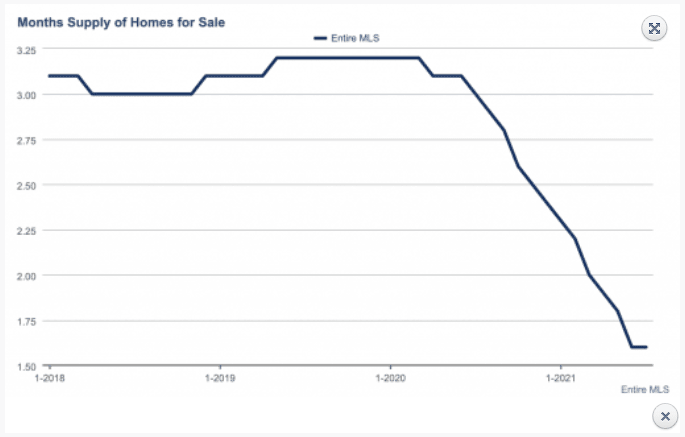

The supply chart below shows supply levels since 2006. In 2007, supply levels peaked at 19 months during the recession. At that point, inventory levels were 3x normal levels and demand was low. In contrast, this past year’s inventory levels are about half of normal while demand, bolstered by the pandemic, has been at an all-time high. That combination has dropped supply levels in half from 3.2 months (pre-pandemic) to 1.6 months. Supply levels have bottomed and are back on the rise. The market with its out-of-balance supply and demand is easing toward balance. Look for seasonal trends to slowly return (including a burst of fall sales activity) for supply levels, market pace, and prices as the market normalizes.